Hello friends,

The obvious topic of the last few day has been Japan’s market crash – one of history’s most violent selloffs. The Nikkei 225 (below) dropped 26.5% over 16 trading sessions, with 18.3% in just two sessions, and broke the 50DMA, 200DMA, intermediate-term uptrend-line, long-term uptrend-line, and even fell temporarily into bear market territory.

The move comes along a (not really surprising) change of gear by the BoJ regarding the ever-easy money in Japan, and is potentially intertwined with negative sentiment from the American economy. It will remain to be seen whether this is the end or the beginning (back into bear market territory) of the move – economic contraction has not been visible there yet, but the market starting to price in reduced financial liquidity via the money markets could easily start a new bear market. We will see – for now, all I see is a whole lot of broken stocks, no leaders, and a lot of short setups.

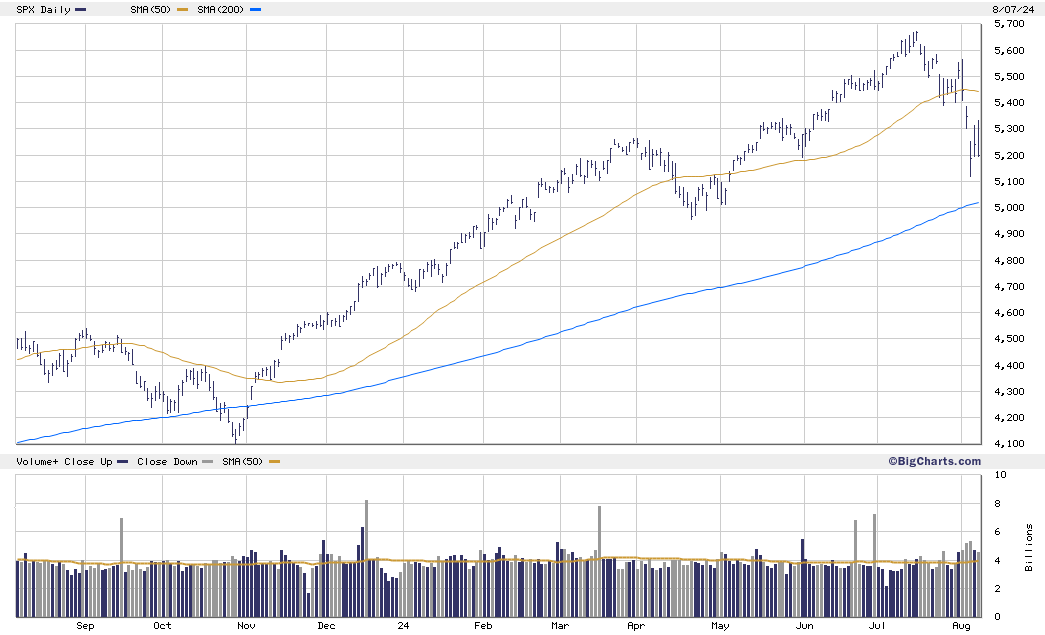

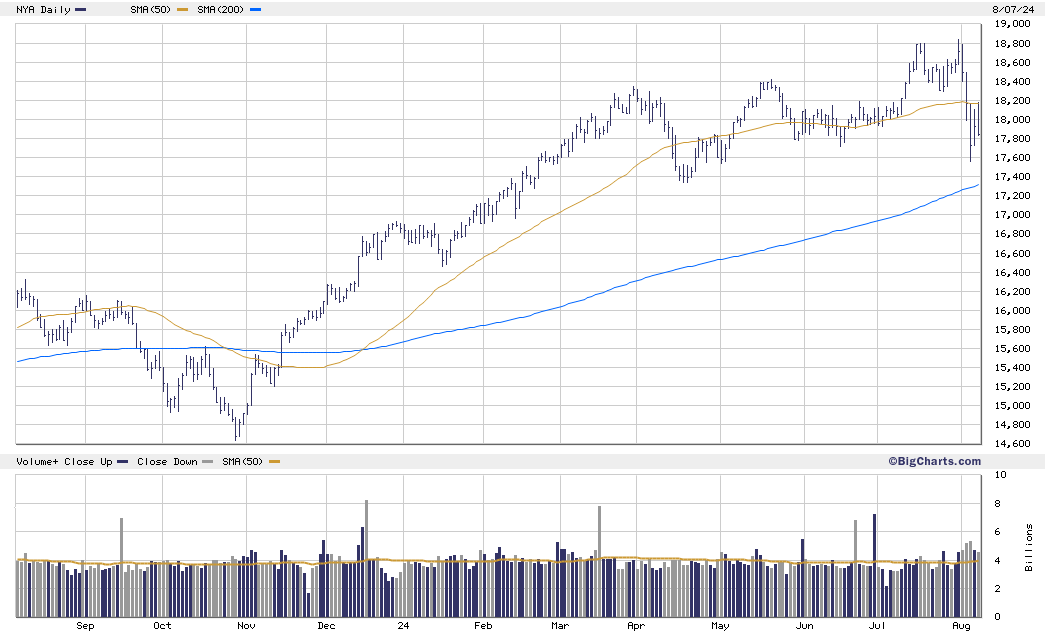

The US and EU indices have been mirroring, and in many cases front-running this behaviour, though on a much less dramatic scale. Cap- & equal-weighted versions of the SP500 (SPX, below) and NASDAQ-100 sold off below intermediate uptrend-lines, whereas the more uniformly moving NYSE Composite (NYA, below), SP400 Mid-Caps and Russell-2000 Small-Caps all rejected their recent breakout moves violently. So far, as I indicated last report, the violent up-move at the beginning of July might have been nothing but a short-covering rally on the heels of the latest CPI report, while the market now seems to be broadly disagreeing with the Fed’s problematic decision to delay interest rate cuts into September. The whole rally starting November ’23 was largely anticipatory of these cuts, and now we appear to be seeing another money rotation in a sell-the-news dynamic.

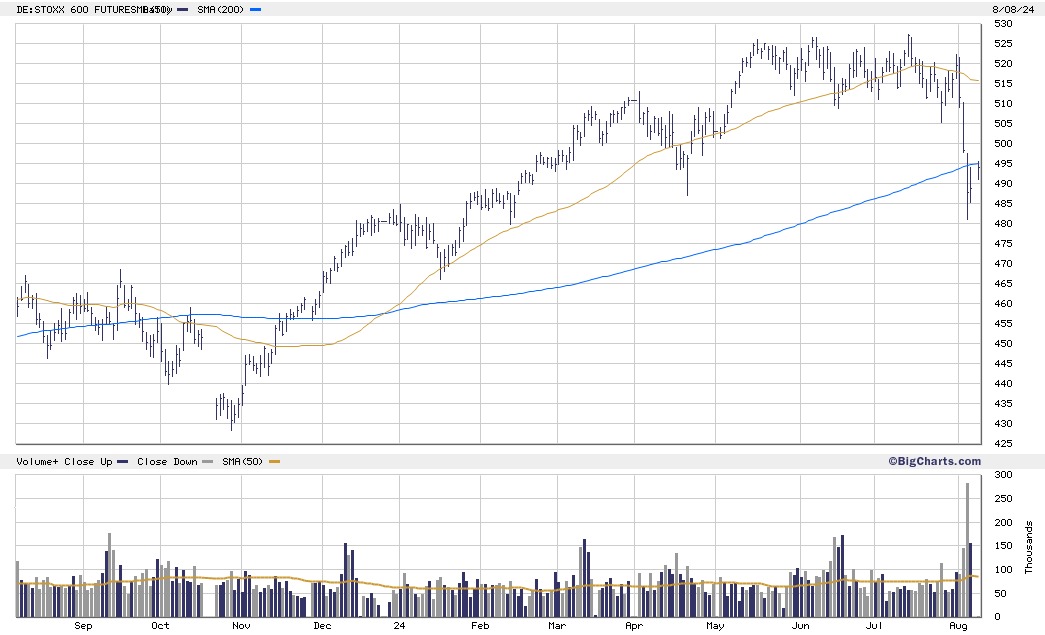

US (SP500) and EU (Stoxx 600, below) equities are now showing stalling action and have entered secondary corrections – which might or might not lead to a broader bear market. The VIX has spiked dramatically to over 60% intraday on Monday, indicating the start of wild de-risking behaviour by large institutional money.

Paired with weakening labour markets, contracting manufacturing sectors (see the June ISM PMI), strongly receding commodity markets, low producer- and consumer sentiment, and yield curves looking to un-invert, markets might now start to forecast a contraction, or at least slowdown, of their respective economies. In reality, real GDP growth has been nothing but weak-magnitude propped up by excessive government spending since COVID across the West, explaining at least partially the thin nature of the 2023-24 rally.

The only group move worth mentioning in my eyes for long positions is healthcare, specifically biotech. There are a myriad of strongly-behaving stocks across the US and EU. For example, check out INSM (currently forming a high tight flag), DYN or RNA in the US, or GUBRA.CO and ZEAL.CO in Denmark. Very strong moves, low sensitivity to the general market declines. If you need additional long exposure, this is where to go.

Take GUBRA.CO as a prime example to reflect current market atmosphere: Significant returns can be had when pyramiding into large positions, but they come at a cost – volatility has been and remains high, as you can see with the massive whipsaw on May 13/14, shaking out a lot of traders. Stops need to be widened and position sizes cut down, leading to diminished risk/reward profiles. This is just the nature of the beast right now, and we’ll have to accept it. Stay flexible, go with the trend, and remember to be careful right now – the VIX might drop (or not), but individual stock volatility might as well stay even more so elevated.

So long,

TGS